SignalPlus宏观分析特别版: Negative Revisions

3 hours ago

Original author: Castle Labs

Original translation: AididiaoJP, Foresight News

Over the past 12 months, stablecoins have steadily moved from a marginal role in the crypto world to the broader financial market. The data speaks for itself: stablecoin supply has more than doubled, and usage among traditional payment networks and institutional participants has surged, demonstrating growing interest in these assets. But a deeper shift lies at work: what was once a place for crypto traders to park their profits has become a transaction layer in emerging economies, a settlement tool within fintech stacks, and a strategic monetary extension of US monetary policy.

This report compares stablecoin usage from mid-2024 to mid-2025, tracking growth in adoption, regional shifts, and the current status of stablecoins as a product and concept.

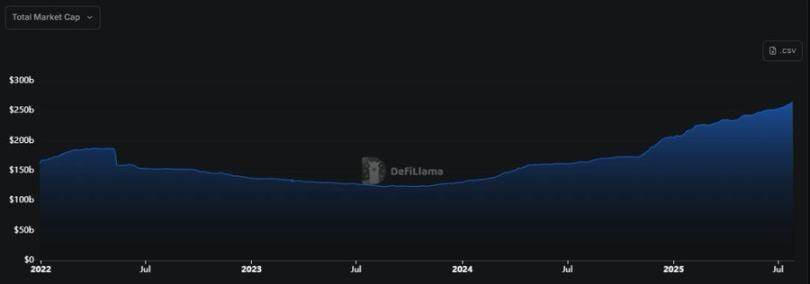

The market capitalization of stablecoins rebounded from approximately $160 billion in mid-2024 to over $260 billion in July 2025, an increase of more than 60%, pushing the total amount of stablecoins in circulation beyond the 2022 high and setting a new liquidity record.

On-chain transaction volume is even more telling. In 2024, stablecoin settlement volume surpassed Visa and Mastercard combined, reaching $27.6 trillion. Monthly transaction volume doubled year-over-year, from $1.9 trillion in February 2024 to $4.1 trillion in February 2025. Peaking at $5.1 trillion in December 2024, it demonstrates that these funds are no longer limited to the crypto-native sector; in some ecosystems, stablecoins account for over half of all transaction value.

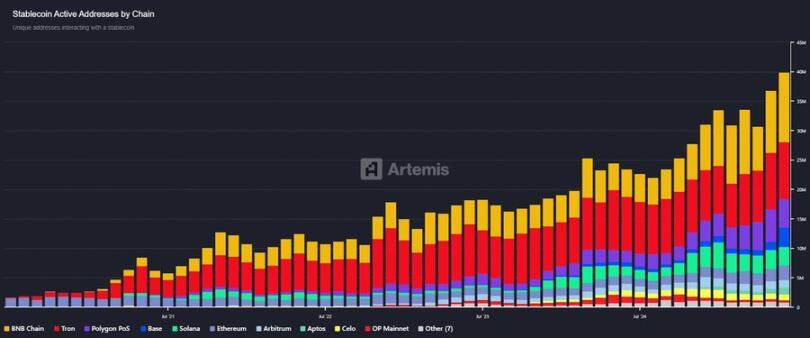

The number of active wallets will grow from approximately 20 million in mid-2024 to approximately 40 million in mid-2025. The total number of addresses holding stablecoin balances has exceeded 120 million. This growth is not only quantitative but also reflects diversity. A growing number of small businesses, freelancers, and remittance users are using stablecoins to transfer funds, often without direct participation in the broader crypto market.

By 2024, stablecoins will have become a financial tool not only for crypto companies but also increasingly adopted by fintech firms, asset managers, and some enterprises. The reason is simple: they offer a fast, programmable, dollar-denominated asset that can be transferred across platforms at any time, without relying on traditional banking channels. For companies operating across multiple countries or time zones, this means improved liquidity management, faster internal transfers, and reduced settlement delays.

With interest rates expected to remain high for most of 2024, it's even more appealing to park idle cash in stablecoins like USDC. Many stablecoins are backed by short-term government bonds. While users don't directly earn a return on their holdings, their reserve structure provides confidence that the underlying assets are high-quality and interest-bearing. This makes stablecoins a viable option for companies seeking a reliably backed digital alternative to the US dollar.

This year, stablecoins have become more deeply integrated into fintech infrastructure. Visa expanded USDC settlements to Ethereum and Solana. Stripe and PayPal introduced stablecoin payments to consumer channels. Even banks have begun testing local stablecoins, such as Standard Chartered's HKD coin, to explore faster cross-border settlements.

Tether's $13 billion profit in 2024, more than double BlackRocks', underscores the financial significance of the reserve model. This not only demonstrates that stablecoin issuers are supporting the infrastructure but also that they operate highly profitable businesses. This profitability translates into sustainability, fostering user trust and accelerating adoption across the financial sector.

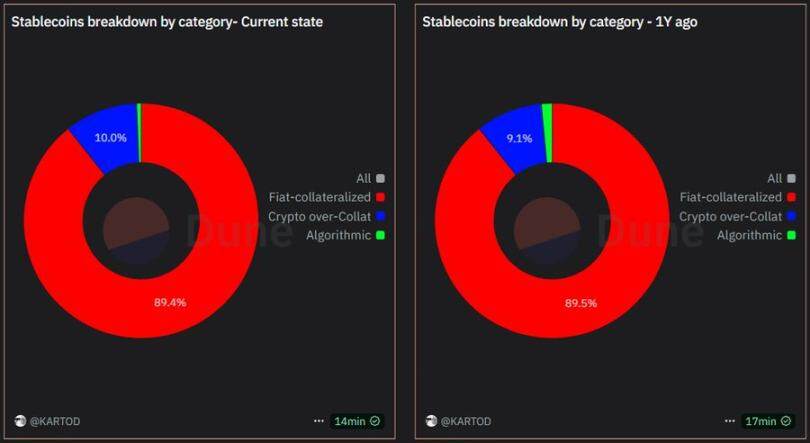

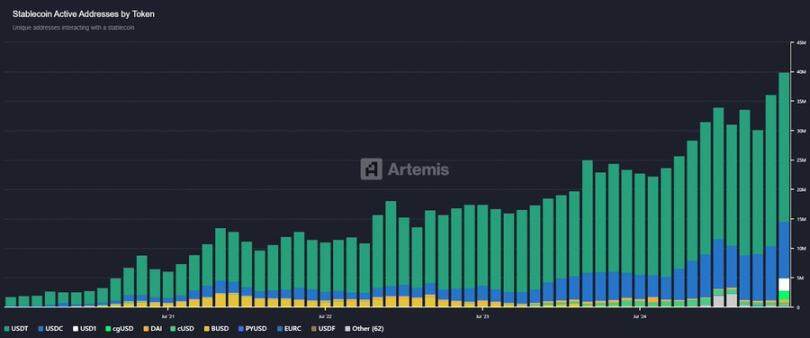

The market share of fiat-backed stablecoins (those fully backed by cash or short-term Treasury reserves) has grown from approximately 85% in 2024 to over 90% today. Tether (USDT) supply has grown from approximately $83 billion to approximately $150 billion. USDC has recovered from its 2023 low of approximately $59 billion and is regaining institutional favor.

Stablecoin adoption has been more modest for stablecoins like PayPal’s PYUSD and Paxos’ USDP, but real growth is concentrated in leading products. User preference for fully backed and transparent reserves has become a widespread expectation, despite the trade-offs of centralized custody and regulatory risks.

Crypto-collateralized stablecoins like DAI have seen slight growth in absolute volume (around $5 billion) but have lost market share. Protocols like Aave (GHO) and Curve Finance (crvUSD) have added hundreds of millions in circulating supply, but crypto-backed stablecoins haven’t truly broken out, nor have they collapsed.

On the other hand, algorithmic models have all but vanished. After the Terra debacle, trust in non-overcollateralized designs was lost, and many projects, including Frax Finance, switched to a fully fiat-backed model in 2023. Since then, no new algorithmic stablecoins have gained significant traction.

Today, fiat-backed stablecoins dominate in terms of usage and consensus. Crypto-backed stablecoins are a small but useful niche market. Algorithmic approaches, once considered mainstream, have largely retreated from the market.

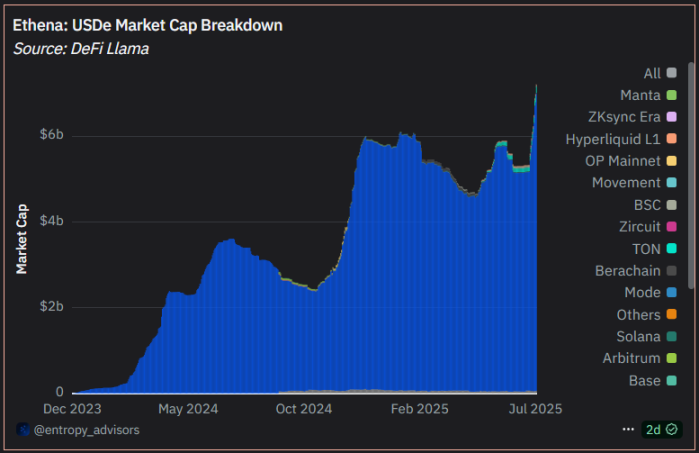

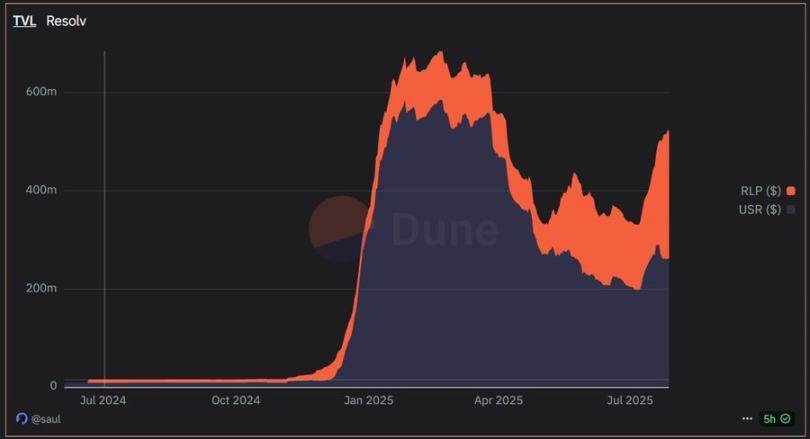

An emerging category worth watching in 2025 is yield-based stablecoins, assets designed not only to preserve value but also to increase it. Unlike traditional fiat-backed or overcollateralized models, these tokens explicitly integrate returns from real-world or on-chain strategies into their structure. Two prominent examples are Ethena's USDe and Resolv's USR.

Ethena Labs' USDe employs a delta-neutral strategy, maintaining its peg by staking ETH collateral paired with a perpetual short position while generating synthetic yield. This yield is passed on to holders via a separate token, sUSDe. This model garnered early attention for its composability, transparent yield mechanism, and ability to generate income without relying on centralized reserves. As of mid-2025, USDe's supply remains significantly lower than that of major stablecoins, yet it remains one of the few projects to achieve significant adoption and maintain stability in the post-Terra experiment.

In contrast, Resolv Labs pegs its returns to real-world interest-bearing assets, creating a structure more akin to a tokenized treasury bond but in the form of a stablecoin. USR aims to maintain its peg while providing users with a stable yield through partnerships with off-chain credit and structured products. This is a more institutional approach, with adoption primarily concentrated among DeFi protocols and early-stage lending platforms.

These models are still in the experimental phase, with adoption rates far lower than those of fiat-backed stablecoins. However, they represent a clear trend: users demand not only stability but also passive yield. The challenge remains maintaining transparency, anchor stability, and regulatory clarity. If any of these falter, confidence will quickly fade.

Yield-generating stablecoins have already established themselves. They haven't replaced USDT or USDC, but they expand the design space, offering more capital-efficient options for users willing to accept varying risk profiles. Whether they can scale without inheriting the vulnerabilities of previous algorithmic stablecoins remains to be seen. But for now, they are more worthy of attention than any attempt since the UST debacle.

Motivation: Stability and gaining USD exposure

In countries facing inflation and currency volatility, stablecoins are increasingly becoming an alternative to digital dollars. Argentina, Venezuela, and Nigeria are examples. When local currencies depreciate in 2024, demand for USDT surges. By 2025, holding digital dollars has become commonplace for individuals and businesses.

In Africa, where foreign exchange shortages affect over 70% of countries, stablecoins are becoming a bridge connecting local economies with global capital. Nigerian exchanges often quote prices in USDT. When banks are unable to provide US dollars, businesses use stablecoins to pay overseas suppliers.

Remittances and Payments

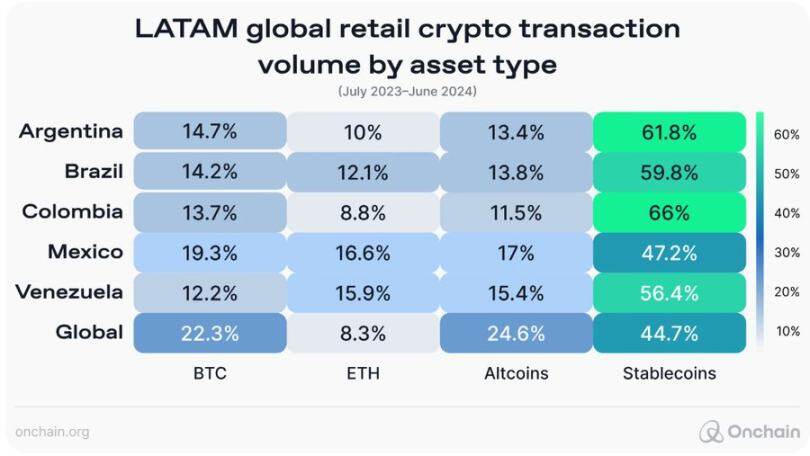

The shift in remittances toward stablecoins is significant. By 2024, cross-border cryptocurrency transfers in Latin America will grow by over 40%. By 2025, apps like Binance P2P and Airtm will have become the primary remittance tool for the entire community.

The average cost of sending $200 in Sub-Saharan Africa via stablecoins is approximately 60% lower than via traditional remittance channels. This isn’t a marginal improvement, but a demonstration of transformative impact and product-market fit.

Preferred Platform and Token

Tron has become the dominant public blockchain for stablecoin activity in emerging markets due to its low fees, with most niche and peer-to-peer markets using USDT on Tron. Bitcoin Scenario (BSC) and Solana have also gained market share, but Tron remains the default choice in many regions.

USDC is gradually penetrating traditional financial payment channels, especially when regulatory scrutiny or institutional relationships become a concern. However, for ordinary users, USDT still holds an absolute advantage.

Regulatory attitude

Governments remain cautious. Brazil has introduced digital asset regulations and is exploring central bank digital currencies (CBDCs). South Africa is developing guidelines for stablecoins. Most other emerging markets remain on the sidelines. While recognizing their utility, they also worry about dollarization and capital flight. For now, basic use is tolerated, especially in the absence of alternatives.

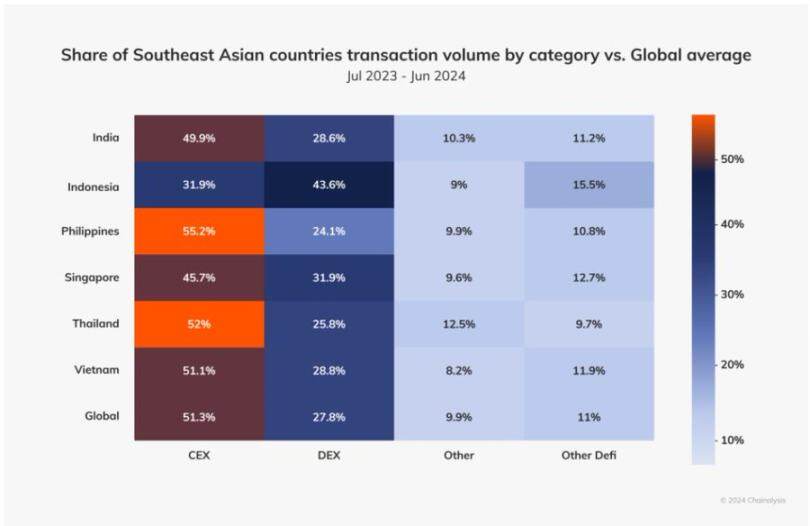

Southeast Asia and South Asia

In Southeast Asia, stablecoin usage is more about access than inflation. In countries like the Philippines and Vietnam, remittances are a primary driver. Overseas workers send USDT or USDC back home through apps like Coins.ph or BloomX. In India, traders and freelancers use stablecoins to transfer funds between platforms and reduce slippage.

Vietnam stands out in retail crypto adoption, while Singapore takes a more institutional approach, granting stablecoin licenses and encouraging regulated issuance.

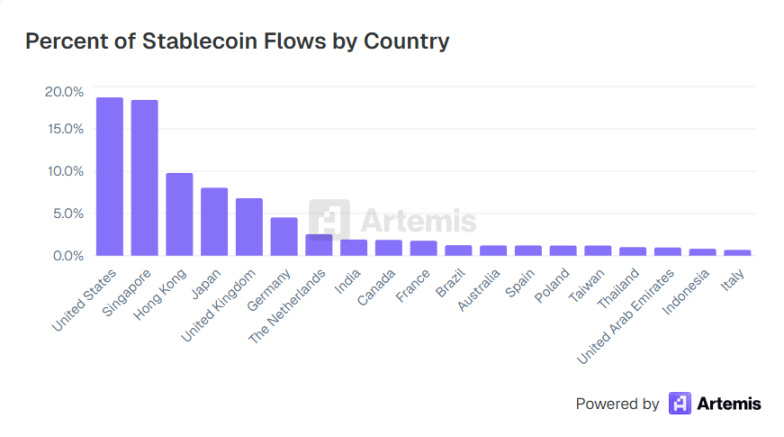

East Asia and Financial Center

Hong Kong and Singapore are positioning themselves as regulated stablecoin financial hubs. The Monetary Authority of Singapore (MAS) has implemented clear guidelines (reserve backing, redemption terms) by the end of 2024. USDC and regional stablecoin issuers are applying for Singapore licenses by 2025.

Japan will allow banks to issue stablecoins under a legal framework established in 2023. Several yen-pegged stablecoins already exist, but they remain niche. In South Korea, due to strict regulations, stablecoin use remains concentrated in the trading sector.

While cryptocurrency-related activities remain officially prohibited in mainland China, USDT is widely used over-the-counter (OTC) channels. Reports indicate that significant capital flight and trade flows are occurring through Tether on Tron. This is a persistent, yet unofficial, phenomenon.

In the United States and Europe, stablecoins are rarely used for everyday consumption, but are embedded in the backend of fintech stacks, corporate finance, and cross-border settlements.

Companies use stablecoins to transfer funds between subsidiaries. Freelancers accept USDC for international work. Following the 2023 bank collapse, crypto companies now rely on stablecoins rather than ACH or SWIFT for fiat transactions.

Franklin Templeton's on-chain money market fund is settled in USDC. Mastercard and MoneyGram have launched stablecoin-based services. These integrations demonstrate the complementary expansion of stablecoins in fintech, rather than their full potential as a replacement.

The EU's MiCA framework will take effect in mid-2024. Non-euro stablecoins will face daily caps by mid-2025, and issuers will need to apply for licenses. The UK has also passed legislation recognizing stablecoins as digital settlement assets.

In the United States, the GENIUS Act has just been passed, but its impact has yet to be felt. Previous enforcement actions (such as the decline of BUSD) and market behavior (focused on USDC/USDT) suggest that regulators are indirectly shaping the sector, but this situation is changing. Stablecoins now account for over 1% of the M2 money supply, a fact that Federal Reserve officials have begun to publicly acknowledge.

Between July 2024 and July 2025, stablecoins transitioned from being primarily crypto-native tools to becoming independent, parallel financial systems. In emerging markets, they became a solution to circumvent currency collapse and expensive banking services; in developed markets, they were integrated into regulated, compliant workflows.

Market structure reflects this evolution. Fiat-backed stablecoins dominate, holding over 90% of the market. The algorithmic and unbacked models once considered central to "decentralization" have largely vanished. Stablecoin usage is now driven more by practicality and trust than ideology.

The regulatory environment hasn't fully caught up, but it's progressing. Institutions, banks, fintech companies, and payment giants are gradually adopting stablecoins. The question now is not whether they will be regulated, but how they will be regulated and integrated into existing organizations, and how much value they will hold and where that value will flow.

Stablecoins are unlikely to completely replace fiat currencies, but they are already filling gaps in areas where traditional currencies fail, such as after-hours, cross-border scenarios, or economies with weak infrastructure.

Future developments will depend on continued utility, clear rules, and the ability to scale benefits without compromising stability or transparency. But looking back over the past year, the trend is clear. Stablecoins have found a role, and it's one that's more significant than most anticipated.