Original post by: Biscuit, Chain Catcher

While Aave was in full swing to formulate the specific parameters of the GHO stablecoin, MakerDAO announced that it might choose to sell all USDC exposure in the protocol. This is undoubtedly a blockbuster that may redefine the standard of decentralized stablecoins.

According to the Yearn core developer banteg'sstatement, MakerDAO may buy $3.5 billion in ETH, converting all USDC from pegged stable modules to ETH.

MakerDAO's original design was based on an over-collateralized stablecoin protocol based on ETH, but it was able to tide over the difficulties by urgently introducing USDC during the "312" black swan incident, and at the same time lost its identity as a purely encrypted protocol.

Circle froze USDC held in Tornado Cash wallet addresses after the U.S. Treasury Department blacklisted Tornado Cash. This means that users who deposit USDC into Tornado Cash may not be able to withdraw their funds. This makes all encrypted users panic: Oh, it turns out that the decentralization we are proud of is so vulnerable.

MakerDAO community members@TetranodeOnce the largest liquidity provider of the agreement, he left angrily after the agreement decided to introduce USDC. Today, he believes Circle is helpless in the face of regulators, and the crypto world should explore stablecoins that don’t depend on real-world redemptions.

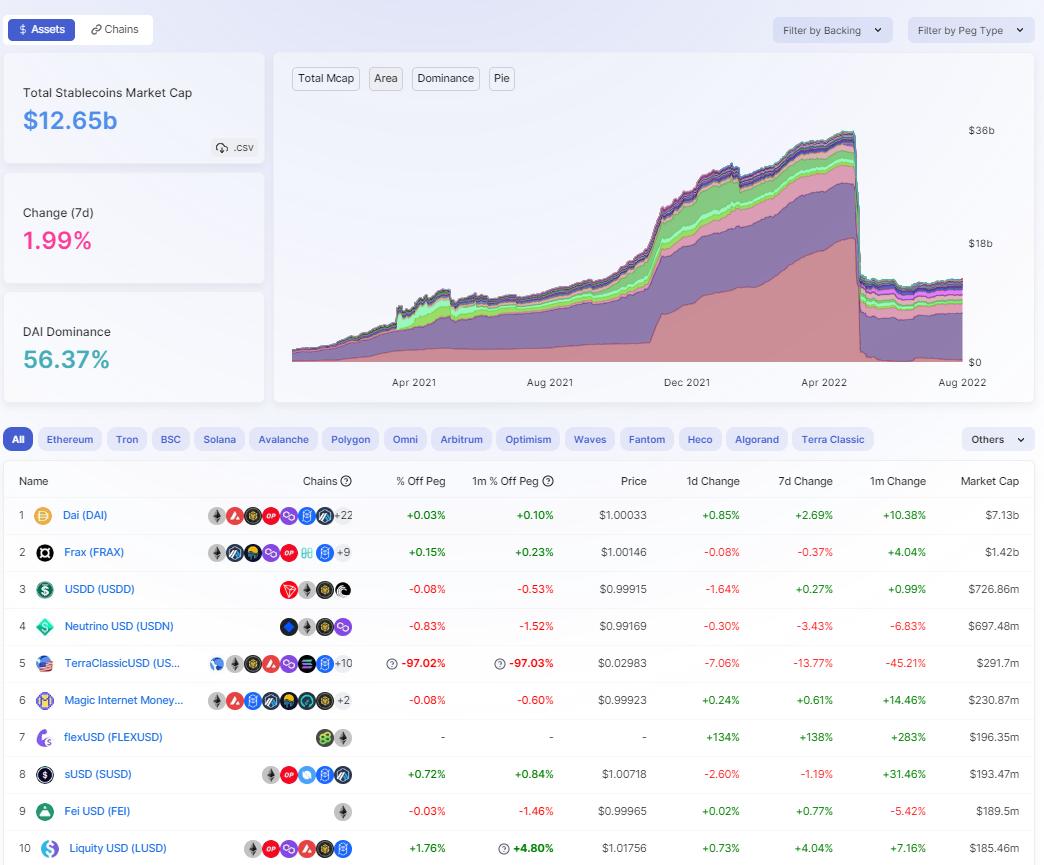

According to data from CoinGecko, the total market value of stablecoins is about $153 billion, accounting for more than 13% of the total market value of cryptocurrencies, which is also the highest level in history. Centralized stablecoins (USDT, USDC, BUSD) account for as much as 90%. The crypto world seems to have been hijacked by centralization.

first level title

The Quadruple Dilemma of Stablecoins

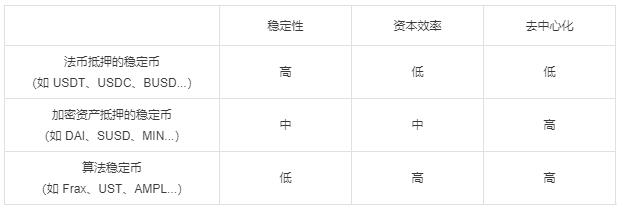

Compared with the "impossible triangle" of the public chain, stablecoins also have their own triple dilemma, namely price stability, capital efficiency and decentralization. Therefore, many encryption teams will focus on a certain feature when designing stablecoins, making their stablecoin protocols more narrative.

Fiat-collateralized stablecoins (such as USDT, USDC, BUSD...): Mortgage fiat currency assets (such as U.S. dollars, euros, etc.) to issue stablecoins, each of which is backed by real U.S. dollar value 1:1.

Stablecoins collateralized by encrypted assets (such as DAI, SUSD, MIN...): Pledge encrypted assets (such as BTC, ETH, etc.) to issue stablecoins, usually in the form of over-collateralization.

Algorithmic stablecoins (like Frax, UST, AMPL...): Rely on complex algorithms to balance the supply and demand of stablecoins to keep prices stable through smart contracts.

In addition, some emerging NFT protocols are also trying to issue stable coins. For example, JPEG'D draws on MakerDAO's CDP (collateralized loan stable currency) model, and users pledge NFT to lend stable currency PUSD.

Countless crypto teams have attempted to challenge the throne of decentralized stablecoins, and most have failed. These courageous social experiments are not without merit, and we can extract feasible and successful experiences from these various solutions.

MakerDAO is the most successful decentralized stablecoin protocol. Its advantages include support for multiple collateral types (including real-world assets RWA), adjustable lending rates, four-tiered liquidation mechanism, PSM module, and Flash that allows users to quickly mint DAI Mint modules and more.

Bolder innovations are happening with algorithmic stablecoins, such as the hybrid algorithm stablecoin FRAX uses part of the hard currency asset mortgage to improve capital efficiency, and uses the algorithmic market controller AMO to balance market circulation. Ampl issues the stable currency perpetual note SPOT to hedge against AMPL's supply fluctuations. RAI's PID control module implements bivalent mode and more.

Although these successful experiences have limitations, it is undeniable that they will serve as a skill pool for decentralized stablecoins for designers to choose flexibly when necessary.

In addition to the triple dilemma, the regulators have paid special attention to stablecoins, and the compliance (availability) of collateral has become a hidden fourth dilemma.From a traditional perspective, the “central bank” that issues stablecoins is the driving force behind all encryption activities, so regulators hope to strengthen the supervision of stablecoin issuers.

Libra, the stable currency project of the Internet giant Facebook, also died because it could not escape supervision. In particular, the collapse of the Luna/UST pure algorithm stable currency of the Terra series caused the evaporation of 40 billion US dollars, and even caused problems in the real society. The United States, Europe, and South Korea are all in full swing to formulate stable currency bills.

first level title

Head-to-head protocol competition

On April 2, Terraform Labs community members proposed introducing 4pool, the new “gold standard” for stablecoin liquidity. This approach is equivalent to UST directly declaring war on DAI. Beside the couch, how can you allow others to snore and sleep. Everyone knows how tragic the war was. UST lost badly, and the market value of the decentralized stablecoin was cut in half.

image description

secondary title

MakerDAO

MakerDAO has been the central bank of the encrypted world for a long time. The DAI stablecoin it issued ranks fourth among all stablecoins. The highly cohesive community and years of practical experience are the reasons why MakerDAO has become the leader of decentralized stablecoins.

But this decentralized "central bank" also has its own difficulties. According to statistics from DeFi researcher @kermankohli, over the past 180 days, MakerDAO's pure protocol revenue was $24 million, and it may only be able to break even. The buy-and-burn model of the governance token MKR may also be problematic. Over the past 5 years, MKR has only consumed 2.24% of the supply. MKR's value capture capabilities may leave holders behind other protocols.

In addition, MakerDAO's end plan "EndGame Plan" may also drag down the agreement's exploration of stable coins. The plan was proposed by MakerDAO founder Rune Christensen to reorganize the protocol into multiple subDAOs, aiming to get rid of financial losses and apathy from community members. However, when the fist product DAI is no longer tightly held, is it easy to be defeated by the outside world and become a mess?

In order to maintain the monopoly of decentralized stablecoins, MakerDAO is working hard on the L2 network and the real world. According to Defillama data, the circulation of DAI in multiple L2 markets can compete with USDT/USDC. Within 5 days, DAI rose from 30 million to 140 million in Optimism. Even in the Aztec network, DAI is the only stable currency.

secondary title

Aave

GHO is a decentralized stablecoin native to Aave that will be created by users (or borrowers). As with all borrowing on the Aave protocol, users must provide collateral (at a specific collateral ratio) in order to mint GHO. Correspondingly, when a user repays a borrowed position (or is liquidated), the protocol destroys that user's GHO.

Celcius' thunderstorm prompted MakerDAO to disable the D3M module, which is most likely the direct cause of Aave's issuance of the GHO stablecoin. The D3M module is the Direct Deposit Dai Module, which allows users to lend DAI directly from Aave at the highest interest rate. D3M provides Aave with stablecoin circulation and minting discounts, and also brings MakerDAO the benefits of DAI minting. More importantly, DAI can quickly enter other public chains following Aave's multi-chain expansion strategy. This is a win-win cooperation.

Although the specific operating parameters of GHO have not been released yet, it can be seen from the proposal that GHO is similar to DAI in many aspects, such as over-collateralization, decentralization, multiple collaterals, community governance, and so on.

More strikingly, the GHO proposes that "facilitators"The concept of (facilitator), which is based entirely on "credit" to issue stable coins, can generate and destroy GHO without collateral, and the overall exposure to specific vertical industries (ie RWA, over-collateralization, algorithms, etc.) may be very valuable. Aave DAO elects a facilitator through governance, then sets a supply limit of GHO, and the facilitator can be deployed to the chosen market.

secondary title

Curve

Curve is also the leading protocol that will issue over-collateralized stablecoins. The native stablecoins will release more liquidity of Curve and increase its total TVL. Previously, Curve launched a liquidity token 3CRV, which is defined as a combination of DAI, USDC and USDT"3pool"Token.

secondary title

Frax

secondary title

Synthetix

final thoughts

final thoughts

In the long run, centralized stablecoins will continue to occupy most of the market share, algorithmic stablecoins are more like a zero-sum game experiment, and over-collateralized stablecoins will have more room for growth.

Stablecoins may enter the "dual-track" era. Although the centralized stable currency (USDT/USDC) is not innovative, it will try its best to embrace regulation, bring real-world assets to the encryption field, and maintain its dominance in the encryption world. Decentralized stablecoins (DAI, GHO) will serve as the cornerstone of DeFi Lego building blocks, and fully explore the value stability of the encrypted world.

The fundamental contradiction of compliance is that stablecoins want the real world to recognize the compliance and value of their assets, while also remaining decentralized (cannot be manipulated by third parties). Therefore, a truly applicable stablecoin regulatory bill requires more communication between the encryption party and the regulator. A16z also said that it is wrong for encryption critics to use Terra's collapse as a handle to attack stablecoins and the entire encryption industry. Tailored rule-making can support the encryption ecosystem and protect consumers.

We are in the middle of the internal scuffle for decentralized stablecoins, but it is not known how long this process will take. GHO and DAI will definitely become a competitive relationship, and healthy competition can promote the development of DeFi. The war for decentralized stablecoins is essentially a struggle to maintain maximum liquidity and price stability.

In addition, the hard fork caused by the merger of Ethereum will also have an impact on all DeFi protocols, and almost all stablecoin protocols accept ETH/stETH as collateral. For risks such as spot premiums, POW/POS collateral identification, oracle prices, and liquidity that may be caused by hard forks, the stablecoin protocol needs to make plans in advance.